Investment Strategies

Fear Of Fallen (Bond) Angels May Be Exaggerated

There are concerns about whether risks in parts of the corporate bond and credit sector are rising. Such worries may even explain why central banks, such as the US Federal Reserve, have loosened policy over the past 12 months. How to read the situation? Here is a brief comment from Barings.

Talking to economists and wealth managers in recent weeks, it

is clear that they are concerned about cracks opening up around

the riskier end of the corporate bond market. It is a factor

sometimes cited for why the US economy, and the wider world,

faces some risks this year. Regardless of the truth of such

worries, it is timely to carry an article exploring the

field.

This article comes from David Mihalick, Barings’ head of US

public fixed income and head of US high yield. The usual

editorial disclaimers apply to contributions from non-editorial

staff; we urge readers who want to comment and jump into the

debate to do so. Email tom.burroughes@wealthbriefing.com

and jackie.bennion@clearviewpublishing.com

Many headlines over the last year have called attention to the

growth of the lower-rated BBB portion of the investment grade

market - and predicted a wave of fallen angels to high yield. But

in that timeframe, we have seen more HY companies upgraded to IG

than the other way around.

Biggest risk

One of the biggest potential risks facing fixed income markets is

that current valuations are not reflecting the potential for an

economic slowdown. As we wrote in a recent blog post, a near-term

recession is not our base case scenario. Nonetheless, there are a

number of macro risks on the horizon—from trade wars to Brexit to

political rhetoric that could impact global growth. It is

plausible that these risks could affect the real economy in a

more substantial way than what we are forecasting based on what

we are currently seeing from individual issuers.

With spreads at fairly tight levels today, particularly in the

higher quality part of the high yield market, any change in

growth expectations could lead to spread widening. While this is

certainly a potential risk, it is not what we view as the most

likely scenario, for a few reasons. From a fundamental

perspective, we believe that corporate earnings and balance

sheets look relatively healthy, and we generally see a strong

consumer in the US driving steady economic growth. Defaults

remain low by historical standards and, while we might see an

uptick in more challenged sectors such as energy, retail and

healthcare, we do not expect to see a widespread increase. We are

also fairly optimistic that some of today’s more pressing macro

issues will reach a reasonable conclusion.

Biggest opportunity

In the high-yield market, one of the most interesting

opportunities we see is being driven by the bifurcation in the

market - which we discussed in our recent podcast, High Yield:

Rates, Recession and Relative Value. Over the last year, the

higher-rated BB part of the market has outperformed lower-rated B

and CCC credits. As a result, spreads on BB credits today are

somewhat compressed, whereas spreads in the lower part of the

market have stayed relatively wide. Looking at the market today,

we think there are select opportunities in B and CCC credits -

but it’s not a case of just buying the market. In order to find

the hidden gems in the lower rated part of the market, it is

critical to do the due diligence and gain a thorough

understanding of a company, and how it is going to perform going

forward. With the right amount of research, this is where the

opportunities will continue to materialise over the next year, in

our view.

In fixed income more broadly, we are increasingly seeing

opportunities outside of traditional corporate and government

bonds - in areas like collateralised loan obligations (CLOs),

distressed debt and certain parts of the asset-backed securities

(ABS) market. In addition to diversifying risk exposure and

lowering the correlation of the asset classes in the portfolio,

allocations to these areas can offer an opportunity to earn

incremental yield relative to traditional corporate credit.

Bold prediction

There have been numerous headlines over the last year calling

attention to the growth of the lower-rated BBB portion of the

investment grade market - and predicting a wave of fallen angels,

or credits that fall from the lowest IG rating to a high

high-yield rating. It’s important to remember that credit ratings

are not always painting a complete picture of a corporate

issuer’s financial health, but can be more indicative of what

corporate treasurers have been incentivised to do. In recent

years, continued low rates and very little penalty associated

with falling from A to BBB have incentivised companies to add

more leverage. But in many cases, these are high-quality

companies that have the ability to make adjustments to their

balance sheets and deleverage as needed. In this context, one

bold prediction is that despite the headlines, we will not see a

wave of fallen angel credits disrupting the high yield markets in

2020.

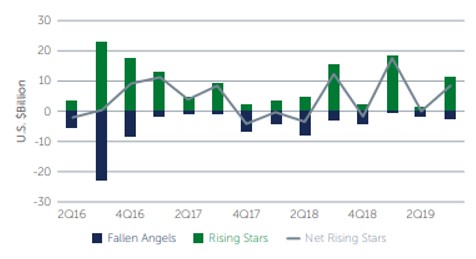

In fact, in the last year, we have seen many more high-yield

companies upgraded to investment grade than the other way

around.

Despite Headwinds, Upgrades Have Outpaced Downgrades in the

US.

US Rising Star/Falling Angel Volume

SOURCE: Credit Suisse. (As of 30 September 2019.

US $Billion.)

Fallen Angels Rising Stars Net Rising